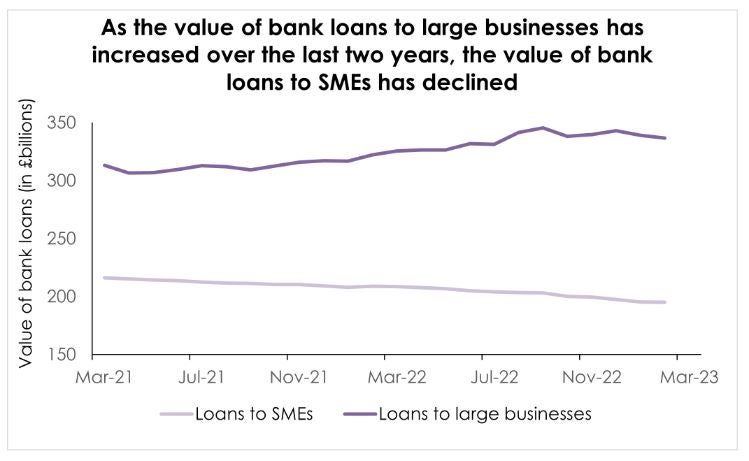

The value of outstanding bank loans to UK SMEs fell by £14bn in the last year, from £209bn to £195bn, according to the Bank of England (BoE), with banking turmoil following the collapse of Credit Suisse and SVB threatening to further reduce access to funding, said ACP Altenburg Advisory, a debt advisory specialist.

The BoE figures are for the year ending February 28 2023.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

In contrast, loans to large businesses increased by £14.7bn, from £322.1bn to £336.8bn, over the same period. These more established businesses with higher turnover are often viewed by banks as lower-risk borrowers than smaller businesses.

Banks started to rein in lending to SMEs more quickly a year ago as interest rate rises began to accelerate. The recent collapses of Credit Suisse and SVB could now make banks even more reluctant to lend, as they focus on reducing risk in their lending books.

Will Senbanjo, Partner at Altenburg, said: “Banks were already reducing their lending to SMEs over the last few years. The recent bank collapses may push them to reduce their risk appetite even more.”

“During times of economic stress, we often see banks pivot away from small businesses in favour of lending to bigger businesses. Until the economic picture starts to become less uncertain, smaller businesses are likely to find bank lending harder to come by.”

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataUK SME bank lending

Another threat to small business lending is a plan to reform bank capital rules in the UK, which economic consultancy Oxera said could reduce lending to SMEs by 25%. The Prudential Regulation Authority’s plan, published in December, removes a key incentive for banks to lend to SMEs. This could result in a major cut to SME lending between 2024 and 2026, according to Oxera.

Will Senbanjo added that businesses with outstanding debts also need to be wary of breaching covenants within their loan agreements. Some loan covenants stipulate that a business’s borrowing costs cannot exceed a specified percentage of its profits. Lower business profitability due to weaker economic conditions would make a covenant breach more likely.

The risk of breaching covenants is exacerbated by the sharp increase to the Bank of England base rate over the last 12 months from 0.75% to 4.25%, which has resulted in the total interest rate charged by lenders increasing sharply for businesses with floating rate debt. A lender may have the right to demand immediate repayment of a loan if their covenants are breached.

Senbanjo said: “Some businesses are likely to be drifting closer to breaching their loan covenants as interest rates rise and the economy continues to struggle. As banks get more concerned about the financial climate, banks are likely to consider tightening lending criteria and focusing more sharply on borrowers that are at or near covenant limits. This could make it challenging for businesses to secure the financing they need to grow.”

Altenburg said that more SMEs will need to seek alternative funding sources to banks such as debt funds over the coming months as the supply of bank lending to SMEs continues to weaken.

UK to be ‘worst performing major economy’ with no growth in February

Cost of living crisis sets back SME plans for Net Zero