The UK government’s plans to part-nationalise the railway sector have raised significant questions about the consequences for rolling stock companies (ROSCOs).

In December 2024, Labour confirmed that South Western Railway would be the first train operating company (TOC) to transition to public ownership in May 2025. SWR is a joint venture between First Group and MTR, the Hong Kong rail operator.

Go deeper with GlobalData

The broader goal is to bring all major national rail routes under public control within five years, thereby reversing one tranche of the privatisation strategy introduced in the 1990s under Conservative Party leadership. While Labour has laid bare its plan to nationalise TOCs, it has retained the existing ROSCO system for rolling stock.

ROSCOs: the financial backbone of rolling stock

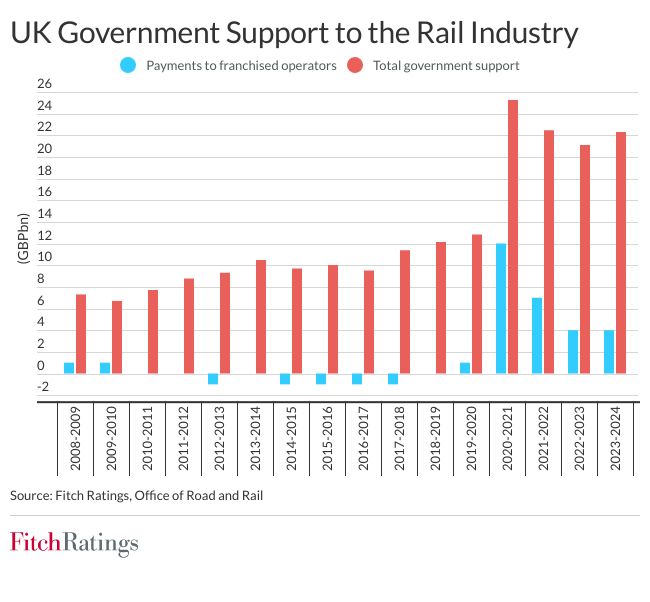

Since privatisation, ROSCOs have been pivotal in financing and leasing rolling stock to operators.

According to the Office for Rail and Road (ORR), as of 31 March 2024, a total of 15,107 railway vehicles were registered for use by passenger train operators. Of these, 71% were electric, 19% diesel, 7% bi-mode, and 3% locomotive-hauled. The average age of the rolling stock across all passenger train operators was 16.6 years.

These private entities own the trains and lease them to operators, a model that has been criticised for imposing additional costs on train companies and passengers.

According to the National Audit Office (NAO), leasing costs now account for 26% of operators’ expenses, with fees nearly doubling in the past five years.

Additionally, the NAO has reported on the financial aspects of the rail system in England. In their publication “A financial overview of the rail system in England,” the NAO notes that rolling stock lease costs have increased by 91% between 2015-16 and 2019-20.

Despite these criticisms, ROSCOs remain profitable, maintaining high margins that have drawn scrutiny from industry experts and passenger advocacy groups alike, not least because of their foreign ownership structures, which mean profits largely go abroad.

The three main ROSCOs in the UK — Angel Trains, Eversholt, and Porterbrook — have attracted substantial overseas investment over the years. Many of these companies are now owned by international investors, and the profits generated from leasing rolling stock are often repatriated to these investors. For example, in the 2020 financial year, the three ROSCOs paid out dividends worth around £950 million, with a notable portion of these dividends going to overseas investors and tax havens like Luxembourg and Jersey.

The Rail Working Group, an industry body, has highlighted the urgency of reducing leasing costs, labelling the situation “critical”. Yet, the government’s current rail reforms stop short of directly addressing the dominance of ROSCOs in the rolling stock market. For a government focused on fiscal prudence, the prospect of purchasing rolling stock outright, which could amount to over £10 billion, remains unattractive.

Eurofima: an alternative financing model

In response to mounting concerns, the government is exploring alternatives, including membership in Eurofima, a supranational organisation based in Basel, Switzerland.

Established in 1956, Eurofima finances rolling stock across Europe for countries as diverse as Sweden, Spain, and Turkey. Notably, it is not an EU institution, with non-EU countries like Norway and Serbia among its members. Its non-profit-maximising approach offers competitive financing rates compared to ROSCOs, whose blended funding costs range between 5% and 7%.

Transport Minister Simon Lightwood has confirmed ongoing discussions with Eurofima, emphasising its potential to support a long-term industrial strategy for UK rolling stock. By joining Eurofima, the UK TOCs could access cheaper financing for new train procurement while avoiding the need to directly include these costs on the government’s balance sheet.

Implications for ROSCOs

The government’s negotiations with Eurofima could have far-reaching consequences for ROSCOs. Fitch Ratings suggests that access to Eurofima’s cheaper funding could put pressure on ROSCOs’ operating margins and dividends, particularly if new procurements are channelled through the planned state-owned Great British Railways (GBR). While existing contracts and the critical role of ROSCOs in the current infrastructure provide some protection, a state-backed lessor with significantly lower financing costs could gradually erode their market dominance.

Challenges and opportunities

Despite these challenges, the UK government is unlikely to fully nationalise existing rolling stock due to the significant financial burden involved. Instead, a gradual fleet replacement strategy through GBR, potentially financed by Eurofima, seems more plausible. Such a move could shift market dynamics, with Eurofima’s funding potentially covering up to a decade of new rolling stock procurement.

The Scottish government’s recent decision to delay the replacement of diesel trains until 2045 offers some respite for ROSCOs. This extension reduces the immediate residual value risk for existing fleets, particularly diesel units. However, it does not materially alter the long-term outlook, as the residual value of diesel fleets is expected to diminish significantly by 2045.

The decarbonisation of ROSCO-supplied fleets ultimately depends on the pace of national infrastructure improvements. While other countries are advancing investments in rail infrastructure, particularly in high-speed rail and electrification, the UK lags behind. According to the Railway Industry Association (RIA), only 38% of the UK rail network is electrified, compared to 57% in mainland Europe.

A crossroads for UK rail

Labour’s pledge for partial nationalisation marks a significant shift in UK rail policy, signalling a move towards greater government involvement in the sector. The potential inclusion of Eurofima in the national strategy offers a cost-efficient alternative to the existing leasing model, potentially delivering savings for passengers and taxpayers. For ROSCOs, however, this development introduces new competitive pressures, emphasising the need for adaptability in a rapidly evolving market.

The global rail industry is forecasted to grow steadily, with demand rebounding after the disruptions of the COVID-19 pandemic. According to the UNIFE Global Market Study, the sector is projected to grow by 3% annually, with the global rail market value rising from €177 billion to €211 billion by 2027. This sustained growth highlights the industry’s resilience and its crucial role in supporting economic development and decarbonisation objectives.

To capitalise on these opportunities, the UK must ensure the wealth generated by its rail sector benefits the domestic economy. Current ROSCO ownership structures, coupled with significant dividend payouts to overseas investors, risk limiting the reinvestment needed to modernise and expand the UK rail network. Redirecting profits towards infrastructure improvements and fostering domestic investment will be essential to securing long-term growth and sustainability.

Eurofima’s involvement in the UK is a welcome development, introducing a degree of competition that can enhance value for money for train operators looking to lease fleets at more affordable prices. By pursuing such reforms and adopting a more balanced approach to infrastructure funding, the UK can strengthen its railways, drive economic benefits, and ensure the sector contributes fully to the country’s environmental and economic goals.